Your Ultimate Guide to Buying a Home in Texas in 14 Steps

Whether you grew up in Texas, are relocating for work, or always dreamed of living in this affable state, it’s a great place to buy a house. Nicknamed the Lone Star state, Texas is the second most populous state in the country and the second largest state in land mass.

“Everything’s bigger in Texas” is a popular slogan and this is true for houses as well. Buyers from other areas, especially New York City or Los Angeles, are often pleasantly surprised by how much square footage and outdoor space you get when buying a house in Texas. Your dollars might stretch much farther here than they do in many other states.

Another plus is that Texas doesn’t have state income tax, according to Rach Potter, who sells homes 44% quicker than the average agent in Dallas, Texas. Texas also has diverse scenery, major cities including Dallas, Houston, and Austin, rolling countryside, beaches, and lots of culinary delights and live music venues.

Steps to buying a home in Texas

Let’s dive into the steps of buying a house in Texas:

1. Assess your readiness and know your financial standing

Before you start looking for homes, you want to determine if you’re ready to purchase one. Consider factors such as how long you plan to be in the area, if you have steady employment, and if you have enough money saved for not just the down payment, but for closing costs, maintenance, property taxes, and more. If you plan on applying for a mortgage, your lender will want to see at least two years of steady employment or business ownership if you’re self employed.

It’s also important to review your credit score and determine if it’s considered excellent, good, fair, or poor. Typically, the higher your credit score, the lower your interest rate will be, which saves you money over the life of the loan. You may want to pay off any collections accounts, dispute errors on your credit report, and pay down your credit card balances before you start shopping for a home.

2. It’s all about the down payment

The median home price in Texas is $435,000 as of June 2022. So, expect to spend somewhere around that number depending on what part of Texas you’re purchasing in, the amenities you want, and the size of the property, among other factors.

Different loan programs will require different down payment amounts, but you do not always need to put 20% down when buying a home. There are loan programs out there that allow for buyers to make low down payments on their dream homes. Some conventional loans allow for first-time buyers to put as little as 3% down, subject to qualification requirements. Putting less than 20% down, however, might require you to purchase mortgage insurance, but it may be worth it to become a homeowner sooner than you anticipated.

FHA Loans usually require a minimum down payment of 3.5% — so if you purchase a house for $325,000, expect to put down at least $11,375 with this type of loan. Keep in mind that this doesn’t include the funds you will need for closing costs.

Before stressing about not having enough money for a down payment, research down payment assistance and first-time homebuyer programs available in Texas to see if you might qualify. It’s best to contact the down payment assistance programs directly for a list of qualified lenders and specific details, as program funding changes frequently.

Consider the following down payment assistance programs in Texas:

- My First Texas Home is strictly for first-time homebuyers, veterans, or buyers who haven’t owned a primary residence within the past three years. They provide assistance up to 5% towards the down payment and closing costs. They work with VA, FHA, and USDA loans and require a minimum credit score of 620. There are some fees involved including loan review and compliance fees.

- My Choice Texas Home doesn’t require that participants be first-time homebuyers and this program works with VA, USDA, FHA, and conventional loans. It also offers down payment assistance up to 5% and requires a minimum credit score of 620, but this program has higher income limits compared with the My First Texas Home program.

- Texas Mortgage Credit Certificate is only for first-time homebuyers, veterans, or buyers who haven’t owned a primary residence in the past three years. This program allows for qualified buyers to receive reductions toward their federal income tax liabilities. Assistance amounts vary and funds are limited.

3. Research the market and determine where you would like to buy

Now that you know more about preparing to purchase a house and down payments, it’s time to decide where you want to live. Do you want to live near family and friends, start over in a new city, live on the coast, or in a more rural area? Consider work commute times, average house prices, and things to do in each area that you’re thinking about living in.

Some great places to consider when buying a house in Texas include:

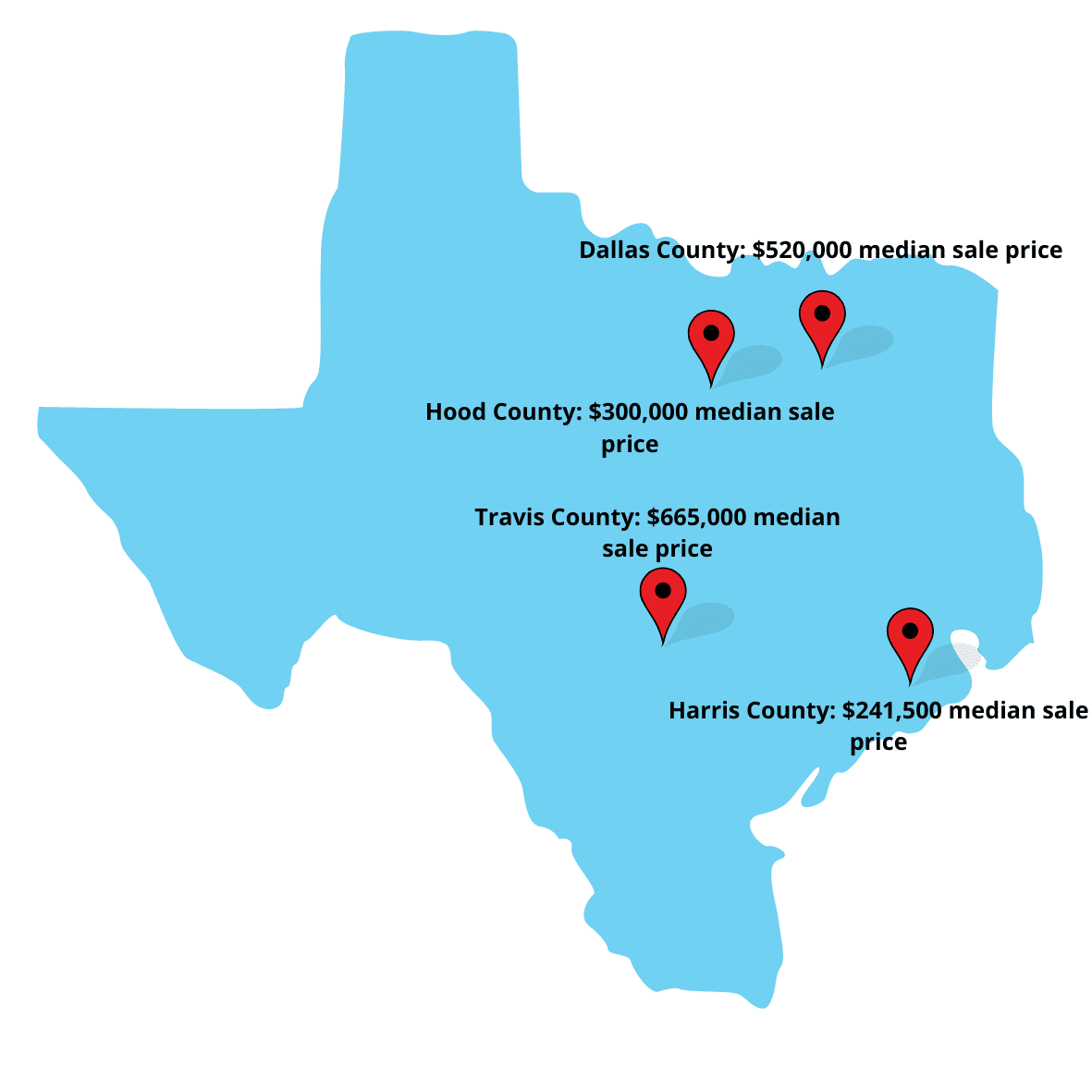

- Dallas county: A popular place to live and includes Dallas as well as Cedar Hill, Addison, University Park, and other nearby towns. It’s the second most populous county in the state and is located in Northeastern Texas. It’s known for its arts district, botanical gardens, and Six Flags over Texas. As of June 2022, the median sales price of homes in Dallas county was $520,000.

- Harris county: Home to Texas’ most populous city, Houston, which is the fourth largest city in the United States. It’s located in Southeast Texas and is near The Gulf of Mexico and Galveston Bay, so there are beautiful beaches and lots of nearby water activities. Houston is home to the famous Lakewood Church and The Houston Rockets basketball team. As of June 2022, the median sales price in Harris county was $241,500.

- Travis county: Home to Austin, Texas’ capital, and is situated in south central Texas. It’s also home to The University of Texas’ main campus. The Austin area is known for its live music scene as well as many parks and lakes ideal for hiking and exploring. As of June 2022, the median sales price in Travis county was $665,000.

- Hood county: An inland area situated in north central Texas. It’s a more rural area and is home to ranches, farmland, wildlife, and one of the best historic small towns in the U.S., Granbury. This town is located on a lake, features a cute historic town center, a nearby vineyard, museums, and a small lakefront beach. The median sales price for a home in Hood county was $330,000 as of June 2022.

4. Get preapproved for a mortgage

Now that you have an idea of where you want to live, whether it be in a bustling metropolis, off of a peaceful prairie, or in a sprawling suburb, it’s time to get preapproved for your mortgage. It’s always smart to shop around for the best rates and terms, but it could be helpful to start with the bank or credit union you already have a banking relationship with. Find out what mortgage products they offer and then compare them to a few other lenders.

You can also ask family, friends, your buyer’s agent, and attorneys for mortgage lender recommendations. When choosing a mortgage lender, ask for a detailed cost breakdown, review the terms you are being offered, and compare loan types.

Once you’ve found a few different lenders to shop with, you will go through a prequalification process. This is different from getting preapproved. It usually doesn’t require a hard-pull on your credit, and instead just gives you an estimate of what you may get approved for based on the information you submit. It can usually be done online in just a few minutes.

The next step will be getting an official preapproval. The lender will check your credit score and you will fill out a loan application listing all of your assets and liabilities (debt). You will be required to provide your proof of employment and income with pay stubs, tax returns, W-2s, or 1099s. Additionally, the lender will ask for other documents such as your bank statements, retirement account statements, and gift letters if you are receiving gifts for your down payment. A preapproval can take as little as one day but could take a few days or longer depending on the complexity of your financial situation.

After you’re preapproved, that doesn’t always guarantee that you will be approved for your mortgage. The lender will be continuously reviewing your financial situation and credit score until your loan goes through the final underwriting process. Now is not the time to make any major purchases, quit your job, or take on any additional debt.

Once you are given the purchase price you are preapproved to buy, it doesn’t mean you have to spend that much on a house either. Consider that the tippy top of your price range.

All lenders have different loan qualifications but most of them will consider the following in making their decision:

- Credit score: This is a number between 300 and 850 that depicts your creditworthiness. Lenders will look at all three credit bureau scores and the higher your scores, the better. A good credit score typically falls between 670 and 739.

- DTI: Your debt-to-income ratio helps the lender assess if you as a borrower would be able to afford your monthly payment. It shows the amount of debt you have in comparison to your income. DTI requirements vary from lender to lender, but conventional loans typically require a DTI of less than 45% — some exceptions can be made for certain qualified borrowers with DTIs of up to 50%. To calculate your DTI, divide your monthly debt payments by your gross monthly income and multiply by 100 to get a percentage.

- Income: Your lender will ask for proof of income and may request tax returns, profit and loss statements, and/or bank statements depending on the source of income. Your lender will typically require a two year history of employment and will require your employer to provide verification of this.

- Down payment amount: Your required down payment will vary depending on the type of loan you get. A higher down payment typically means less risk for the lender, which could translate to a lower interest rate. Your down payment amount determines your LTV, or loan-to-value ratio, which is the amount you owe on your mortgage divided by your home’s value. The more you put down, the lower the LTV.

5. Find a local Texas agent

Real estate agents almost always appreciate it when their clients come to them to start home shopping after getting preapproved for a mortgage. This typically means that a buyer is ready to go and can start making offers. Choose a knowledgeable agent that specializes in representing buyers in the area you want to purchase in.

Your buyer’s agent will be able to help you create a wishlist, set up viewing appointments for you, tell you more about what’s going on in the neighborhood, negotiate on your behalf, and connect you with other vendors such as a title company, insurance agent, and home inspector. Real estate agents are also incredibly knowledgeable on the homebuying process as a whole and can hold your hand throughout the process to keep closing on track.

Find a Buyer's Agent in Texas

Looking for a buyer’s agent to help you buy a home in the Lone Star State? Our platform will match you with qualified agents in your area in just a few minutes.

6. Start shopping for homes

Shopping for homes is supposed to be fun! Start online so you can get an idea of what you like and what you don’t like before viewing homes in person. Check out different styles of homes that are popular in Texas such as ranch homes, farmhouses, mid-century modern homes, Mediterranean, and Craftsman houses. They all have different architectural styles, numbers of stories, and unique details. Determine which one suits your needs, your style, and will make the most sense for how you want to live.

Make a needs list and include characteristics such as number of bedrooms, bathrooms, school district, and neighborhood amenities. Then make a wants list which may include things like a finished basement, a separate shoe closet, or a wet bar. Remember to have patience and don’t get your hopes up too high — no house is perfect, but you will eventually find one that ticks off most of your boxes.

The best time to buy a house can depend on a number of different factors including location, inventory, and number of buyers in the market. If you can avoid “peak season,” you may have access to more inventory and are less likely to be involved in a bidding war. In Texas, peak season is typically in the spring and summer — so if you can wait until late fall and winter, you might be more successful.

7. Make a strong offer

Working with your buyer’s agent to craft a winning offer can sound overwhelming. In competitive markets, cash offers could be more likely to be accepted by sellers with multiple interested buyers. While it is not always recommended to completely waive contingencies to impress a seller, you might consider pairing down to just the inspection contingency and financing contingency to remain competitive. Get creative with your offer — you may want to offer a larger earnest money deposit, schedule a quick closing, or even consider letting the seller rent the house back from you for a certain period of time.

Components of an offer when buying a house in Texas include:

- Purchase price

- Closing date

- Earnest money deposit amount

- Contingencies: Financing, home inspection, and appraisal

- Closing cost stipulations: Who pays for what, and if you’re asking the seller for a credit to use toward closing costs

- Home warranty

- Personal property: Such as appliances or furniture

- Option period: In Texas, this is negotiable, and the buyer can specify the number of days that they have to terminate the contract for any reason. In exchange, an agreed upon non-refundable option fee will be paid to the seller, but the buyer won’t lose their earnest money deposit if they decide to walk away during the option period.

8. Send your earnest money deposit

Your earnest money deposit, also known as a “good faith deposit,” is an amount of money you agree to pay the seller to indicate that you are serious about purchasing the home. This is usually between 1% and 3% of the purchase price. However, a higher deposit can be more attractive to sellers and make your offer stand out in competitive markets.

Whether or not you get your earnest deposit money back if you decide to back out of the sale depends on the contract. If you decide to back out of the purchase for any reason not specified in the contract, you could forfeit your earnest money. Be sure to review the contract with your real estate agent and attorney before making any decisions.

9. Order a title search

Ordering a title search can be done anytime after your offer is accepted, but it’s a good idea to do it as soon as possible because it may take a couple of weeks for the title search to come back, especially if the title company is backed up. Who customarily chooses the title company can vary by state and even county — but if it is the buyer’s choice, your real estate agent or mortgage lender will likely have a recommendation.

The title company will issue a preliminary title report that will be reviewed by all parties including your lender and will include items such as property tax information, easements, CC&Rs, deed restrictions, liens, and any judgments against the title of the home. Any liens, encumbrances, or judgments against the property will need to be removed before the seller can close and convey the property without exceptions to the title.

10. Shop for homeowners and specialty hazard insurances

Homeowners insurance is always recommended and it is almost always required if you’re financing your home with a mortgage. The average yearly cost of homeowners insurance in Texas is $3,429, which is the fifth highest in the nation.

As it relates to insurance requirements, each state will have different recommended coverages depending on what hazards are most common. When buying a house in Texas, most policies cover fire and lightning damage, theft, explosions, accidental water or smoke damage, and vandalism. You should consider adding flood insurance (your lender may require it) to your policy and windstorm and hail coverage, especially if the house is on the Gulf Coast. You may also want to add extra liability coverage and endorsements for things like expensive artwork or jewelry.

11. Order inspections and appraisal

If you’re applying for a mortgage, your lender will most likely order the appraisal and you will pay for it. You will be responsible for ordering your own inspections with the help of your buyer’s agent, again, at your own cost. Your agent can recommend a licensed home inspection company if you don’t have one. The home inspector will schedule a date and time to inspect the house and depending on its size, it may take a couple of hours to complete.

Some common issues in homes in Texas include:

- Foundation issues: This is due to shifting soil because much of the soil is clay, according to Potter. A knowledgeable inspector will be able to notice foundation issues and recommend a structural engineer to examine the foundation and determine if it’s safe or not.

- HVAC systems: These issues arise due to the hot climate and the A/C being run continuously.

- Roof repairs: Extreme weather conditions can cause major issues in Texas homes and roof repairs should be kept up to date and roofs should be replaced when necessary.

- Plumbing issues: Heavy rainfall can disrupt plumbing systems by causing ground movement around the home, therefore damaging pipes.

- Termite/Pests: The humidity can lead to an increase in termites and other pests. You want to get the home tested and treated before major damage is done.

- Radon levels: Although overall radon levels in Texas aren’t considered high, it’s a good idea to err on the side of caution and have a radon test conducted.

12. Negotiate repairs

Remember that everything is negotiable. If you have an inspection contingency in your contract, and the inspection report comes back with tens of thousands of dollars of necessary repairs, it’s time to negotiate.

Talk to your buyer’s agent and come up with a plan for what to ask for during negotiations. Do you want a credit for the leaky roof or would you rather a licensed contractor repair it prior to settlement? If the house needs two new toilets, are you willing to walk away if the seller refuses to budge during negotiations? Keep the bottom line in mind, but don’t nitpick. Home inspectors are meant to be thorough. Focus on major repairs that need to be done ASAP and are going to be costly.

13. Final walkthrough

This is to verify that agreed-upon repairs have been completed and the condition of the home is satisfactory. The final walkthrough is usually done a day or two before the closing date. Your agent will usually accompany you so there are two sets of eyes. Check that all plumbing, electrical, and HVAC units are on and working. If personal items such as the dining room chandelier and the washer and dryer were included in the contract, make sure they’re still in the house.

If you find that the necessary repairs were not made, or that there were damages left behind by the seller, notify your agent immediately so they can rectify the situation before closing.

14. Closing time!

Congratulations, you have made it to the finish line! After final loan documents and escrow documents are signed, and the buyer has wired their down payment and closing costs to escrow, the lender will review and approve the signed documents. The lender will have sent a wire to the escrow company. The buyer will typically get the keys to the property after the closing.

Bottom line

Buying a house in Texas is a life-changing experience and can be a dream come true. Remember to keep a level-head, know how much house you can afford, and work with a team of experts including a real estate agent to make this dream a reality. Keep in mind that no house is perfect, but you can always put your own touches on it to make it feel like home. Don’t bypass inspections, pay attention during the final walkthrough, and enjoy your new home!

Header Image Source: (R K / Unsplash)